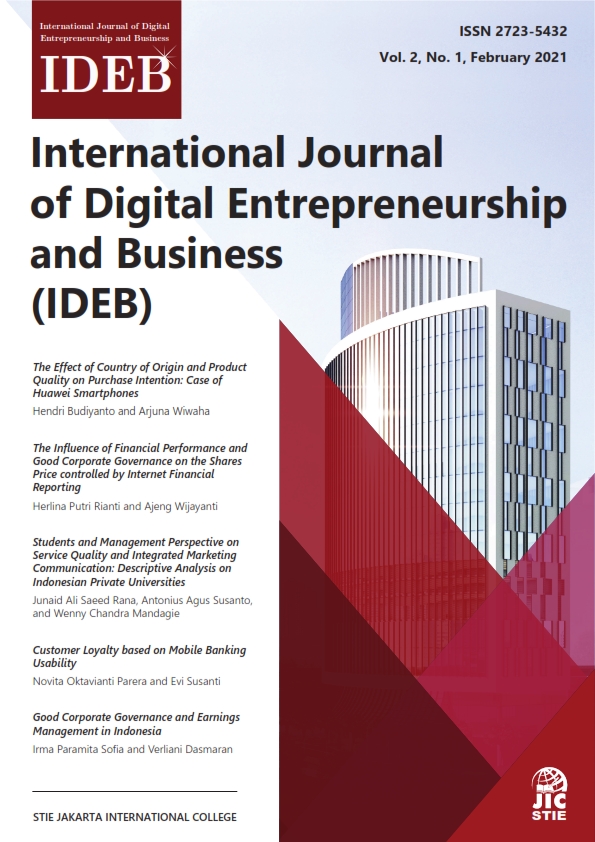

Good Corporate Governance and Earnings Management in Indonesia

DOI:

https://doi.org/10.52238/ideb.v2i1.31Keywords:

Earnings Management, Audit Quality, Audit Committee, Corporate Governance, Manufacturing CompanyAbstract

The purpose of this study was to analyze the effect of audit quality and audit committee on earnings management. The research population is manufacturing companies indexed on the Indonesia Stock Exchange (BEI) in the 2017-2019 period. The sample selection method used was purposive sampling. From population of 180 manufacturing companies, and by selecting certain criteria, a sample of 72 manufacturing companies was obtained. Hypothesis testing is performed using multiple linear regression using statistical software SPSS Version 26. The results of this study confirm that partially, audit quality affects earnings management and audit committee also affects earnings management. Then, hypothesis testing is also carried out simultaneously, and the result is that the quality of the audit and audit committee also affects earnings management. The practical implication of this research is that the quality of the audit and the audit committee can be a reference for investors that can be used as material for consideration in making decisions when investing in potential companies.

Downloads

Downloads

Published

How to Cite

Issue

Section

Abstract viewed = 865 times

Abstract viewed = 865 times